Tesla (TSLA) was in a rough patch in China over the past year, as deliveries softened amid fierce local competition and shifting incentives. Tesla’s mainland retail sales slipped about 5% in 2025 versus 2024, reversing the prior year’s roughly 9% rise that had briefly masked mounting pressure.

That weakness has now begun to look like a turning point after the latest data showed that China-made deliveries from Tesla’s Shanghai Gigafactory nearly doubled in February, jumping 91% year-over-year (YOY) to about 58,600 units, including exports. The surge, helped by an easy comparison to a year-ago production pause for a refreshed Model Y and stronger export flows, signals renewed momentum in the world’s largest electric vehicle (EV) market.

Investors are asking whether this spike signals a true rebound in demand or a short-lived bump. After all, the latest guidance is lacking, and China’s EV market is fiercely competitive.

Tesla Is Betting on Future AI Breakthroughs

Tesla is increasingly shifting its long-term strategy beyond EVs toward artificial intelligence (AI), robotics, and autonomous mobility. While its automotive segment still generates most of the company’s revenue, growth is slowing as Tesla prioritizes autonomy, robotaxis, and humanoid robots as the next phase of innovation. New initiatives such as the Cybercab, Optimus robot, and advanced AI chips suggest Tesla aims to evolve into a broader AI-driven technology platform.

However, this transition brings meaningful risks. If robotaxis and autonomous vehicles fail to scale quickly, Tesla could face a challenging period between 2026 and 2028 as its traditional auto business slows while new revenue streams remain uncertain.

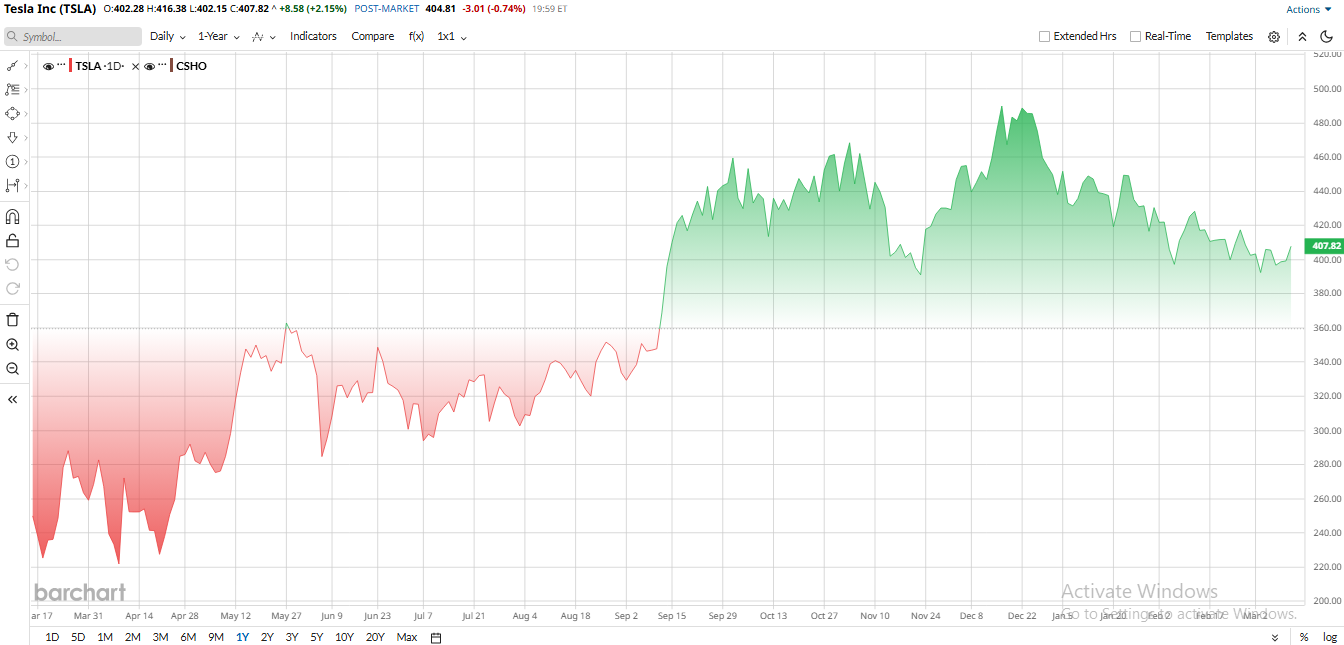

TSLA stock has been under pressure since late 2025. Shares peaked near $498 in December, now trading around the $400 level in mid-March. That marks a roughly 20% drop from the recent high. Despite a 2% rebound on March 11, TSLA stock is down 12% year to date (YTD). Investors can link this underperformance to macroeconomic headwinds, cooling delivery growth, and rising costs.

Even with the recent pullback, Tesla’s valuation denotes a highly expensive stock. For instance, the forward price-to-earnings (P/E) ratio is 283 times, significantly higher than the sector median of 15 times, indicating that shares trade at a premium. Tesla’s premium rating implies that heavy future growth is already priced in.

Tesla China Sales Surge in February

Tesla is showing some negatives in the fast-growing Chinese EV market, and February sales data showed that clearly. Tesla China delivered 58,600 Model 3/Y vehicles, up 91% from a year earlier. Analysts and traders noted that the gain was largely due to a low comparison base. In February 2025, Tesla shut its Shanghai plant briefly for the Lunar New Year, making last year’s numbers unusually soft. Exports from Shanghai also jumped, roughly fivefold year-over-year (YOY) to 20,000 units, as European demand remained strong. Still, Tesla’s China sales were down 15% from January, highlighting normal seasonal swings.

The outlook for China remains choppy as competitors like BYD (BYDDY) cut prices and invest in new models, even as government subsidies taper. In fact, BYD’s China sales fell 65% last month, underscoring market turbulence.

Even so, challenges remain. Global EV competition continues to intensify, and Tesla plans roughly $20 billion in capital spending in 2026 to advance AI, autonomy, and robotics. The company’s long-term strategy increasingly hinges on expanding beyond vehicles into broader AI-driven technologies.

Tesla Tops Q4 Estimates, Yet Sales Decline

In late January, Tesla reported its fourth-quarter earnings print, which normally exceeded analysts’ estimates but saw revenue decline for the first time. Revenue came in at $24.9 billion, down 3% YOY. Every segment equally contributed to this decrease, as the auto business slipped 11% to $17.69 billion, even as energy generation and storage revenue jumped 25% to $3.84 billion. The quarterly decline was driven by slower deliveries — 418,227 vehicles delivered, down 16% YOY — and a tougher pricing environment.

On profitability, Tesla beat expectations on adjusted earnings but saw steep falls in GAAP profits. The company reported $0.50 of adjusted EPS, above the $0.45 Wall Street forecast. Gross margins ticked up modestly to 20.1%, helped by cost efficiencies, but higher operating expenses took a toll. Tesla spent heavily on R&D, and stock-based comp operating expenses jumped 39% YOY.

Free cash flow was anemic by Tesla’s standards. The company generated $1.42 billion in free cash in Q4, well below the $2 billion to $4 billion seen in prior quarters. Still, Tesla ended 2025 with a fortress-like balance sheet. Cash, equivalents, and marketable securities were $44.1 billion, up 21% YOY from $36.6 billion. That liquidity helps fund Tesla’s ambitious capex plans.

Management offered no formal sales guidance, but CEO Elon Musk noted that Tesla will invest heavily going forward. On the earnings call, Musk said the company will “wind down [Model] S and X production” to free up space for robot factory lines, underscoring a shift to new initiatives. CFO Vaibhav Taneja confirmed that capex will far exceed the $9 billion spent in 2025, as Tesla builds six new production lines and beefs up AI compute for projects like its Optimus robot.

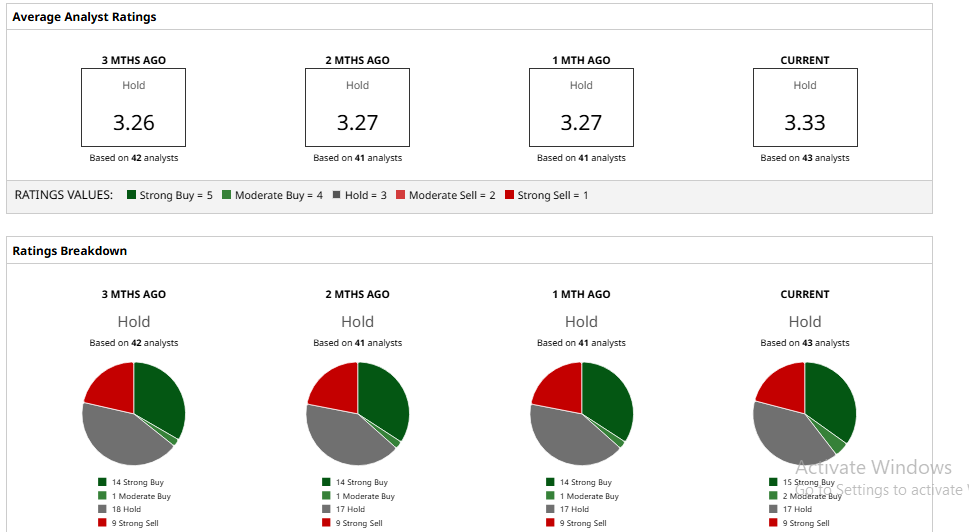

What Do Analysts Think of Tesla Stock?

Wall Street remains divided on Tesla’s outlook. Morgan Stanley reiterated a “Equalweight” rating with a $425 price target. Analyst Adam Jonas argues the long-term prize is a successful robotaxi rollout, and sees full-self driving (FSD) and unsupervised driving as key catalysts for 2027 growth. Jonas forecasts mid-single-digit delivery growth for 2026, implying moderate near-term risk.

By contrast, RBC Capital Markets is bullish. RBC kept its “Outperform” rating and $500 target. Analyst Tom Narayan points to Tesla’s strong balance sheet and $20 billion capex plans next year as reasons to stay positive, noting that Tesla will use its $44 billion cash stash to build six new factories. RBC also believes the robotaxi timeline offers a concrete runway for future growth.

Goldman Sachs is more cautious, cutting its Tesla target to $405 while maintaining a “Neutral” stance. Analyst Mark Delaney highlights Tesla’s shift toward AI and robotics, and acknowledges the huge new capex push, but warns that intensifying competition will keep margins under pressure.

Overall, TSLA stock has a “Hold» consensus rating. The stock is also currently trading near the mean price target of $408.32. However, the Street-high target of $600 set by Wedbush analyst Dan Ives still implies 50% potential upside from here. Ives also believes that Tesla’s valuation could hit $3 trillion by the end of 2026 in the most bullish case, driven by optimism over AI, autonomous driving, and robotics.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

{kind=link}